A recent survey from NewDay USA found that nearly half of all Veterans — 49% — believe buying a home is simply out of their reach right now.

Here’s the thing — a lot of those Veterans are actually much closer to owning a home than they realize. You might be one of them.

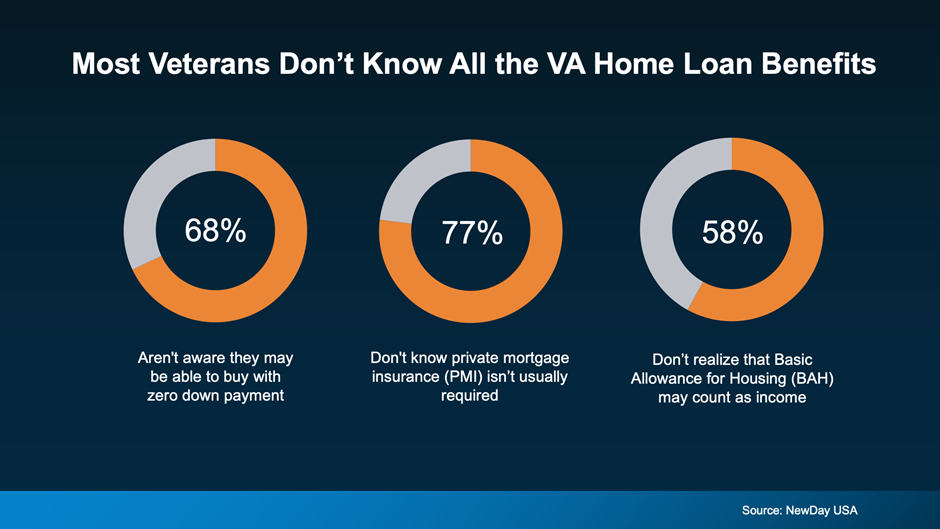

The VA home loan program has been around for more than 80 years, so chances are you’ve heard of it. But knowing it exists and knowing how it actually works are two different things. Three misunderstandings consistently get in Veterans’ way (see graph below):

Any one of those assumptions could be standing between you and a home. Let’s break them down one by one.

No down payment is arguably the most powerful feature of the VA loan — and the most overlooked. In the NewDay USA survey, most respondents assumed they’d need to set aside anywhere from $10,000 to $19,900 before they could even think about buying. That’s potentially years of saving — for a cost that might not apply to you at all.

According to the Department of Veterans Affairs, with VA loans, there can be limits on the types of closing costs buyers have to pay. That means more cash stays in your pocket at the closing table — and less to pull together before you can get there. Stack that on top of the zero-down option, and your path to homeownership can open up faster than you expected.

Most loan programs require private mortgage insurance (PMI) when you put less than 20% down — but VA loans skip that entirely. On a conventional loan, that could mean paying $100 to $300 every single month until you’ve built up enough equity, according to NewDay USA. Add that up over a few years and you’re talking real money — money that stays in your pocket when you use a VA loan instead.

Active duty servicemembers and qualifying reservists have another advantage that often goes uncounted: your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) can factor into your income when qualifying for a VA loan. Since both allowances are non-taxable, they can give your qualifying income a meaningful lift — meaning you might be approved for more than your base pay alone would suggest. If you’ve been running the numbers without them, it’s worth recalculating.

The VA loan benefit exists for a reason — and it’s one of the most powerful tools available to Veterans who want to buy a home. But it only works for you if you actually understand what it covers. That’s where a knowledgeable lender makes all the difference.

Whether you’re currently serving, have served, or you’re supporting someone who has — reach out to a lender who specializes in VA loans and can walk you through the details specific to your situation. You might be a lot closer to buying than you think.

All loans subject to underwriting approval. Certain restrictions apply. Call for details. CrossCountry Mortgage, LLC. is an FHA Approved Lending Institution and is not acting on behalf of or at the direction of HUD/FHA or the Federal government. Certificate of Eligibility required for VA loans. This site is not authorized by the New York State Department of Financial Services. No mortgage loan applications for properties located in the state of New York will be accepted through this site. NMLS3029 NMLS1640418 NMLS460442 (www.nmlsconsumeraccess.org).

Privacy Statement | Disclosures & Licenses | General Disclaimer | NMLS Consumer Access