Student loans are back in the spotlight. Whether you've been following every headline or just catching bits and pieces, there's a good chance they've been on your mind lately.

And if you're wondering whether you have to hit pause on your plans to buy a home, here's the thing I want you to remember:

Having student loans doesn't automatically mean buying a home has to wait.

The Biggest Myth About Student Loans and Buying a Home

I hear this from buyers almost every week: "I can't buy until my student loans are paid off." It's one of the most common misconceptions among first-time buyers, and in most cases, it's just not true.

Here's how it actually works. When I review an application, student loans get evaluated the same way other debts do, like credit cards or car payments. What I'm really looking at is your debt-to-income ratio, or DTI, which compares your total monthly debt payments (student loans included) to your gross monthly income. As long as your DTI falls within acceptable limits, that student loan balance doesn't disqualify you.

So no, having that loan on your credit report isn't some special red flag that shuts the door on you.

Instead, I look at your overall financial picture: your income, your credit history, your savings, and more. Student loans are one piece of that puzzle, but they're not the entire picture.

You're in Better Company Than You Think

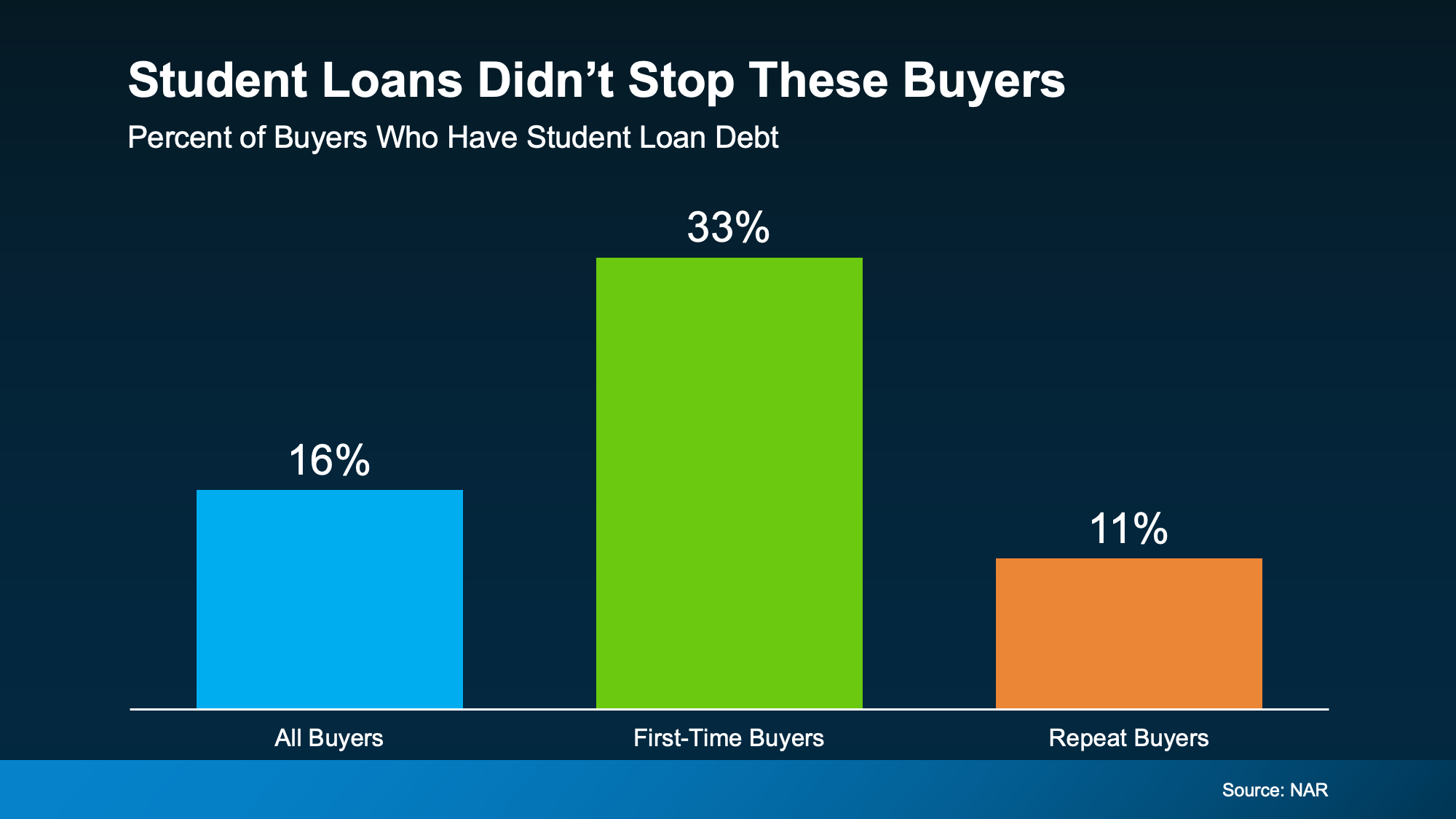

Just to really drive this home, here's a stat from the National Association of Realtors (NAR) that proves you can have student debt and still buy a home. Their research shows 33% of first-time homebuyers still had student loan debt when they purchased.

That's 1 out of every 3 first-time buyers. The median amount they owed? $30,400.

People are buying homes with student debt every single day. Carrying student loans doesn't automatically put homeownership out of reach.

Don't Count Yourself Out Before You Even Try

At the end of the day, here's where I see a lot of buyers trip themselves up: they assume the worst and never even check what they could actually qualify for. They give themselves a blanket "no" before anyone who does this for a living has looked at their numbers.

But your situation is more unique than a blanket "no." If your income is steady and the rest of your finances are in decent shape, buying a home could be more realistic than you think. The only way to know for sure is to run the actual numbers, and that conversation costs you nothing.

You may discover you're closer to buying than you think.

Bottom Line

Student loans don't have to be the thing standing between you and owning a home. If you've been putting off your homebuying plans because of that debt, let's talk through your options. It may not be the barrier you think it is.

All loans subject to underwriting approval. Certain restrictions apply. Call for details. CrossCountry Mortgage, LLC. is an FHA Approved Lending Institution and is not acting on behalf of or at the direction of HUD/FHA or the Federal government. Certificate of Eligibility required for VA loans. This site is not authorized by the New York State Department of Financial Services. No mortgage loan applications for properties located in the state of New York will be accepted through this site. NMLS3029 NMLS1640418 NMLS460442 (www.nmlsconsumeraccess.org).

Privacy Statement | Disclosures & Licenses | General Disclaimer | NMLS Consumer Access